Interest Rates Rising

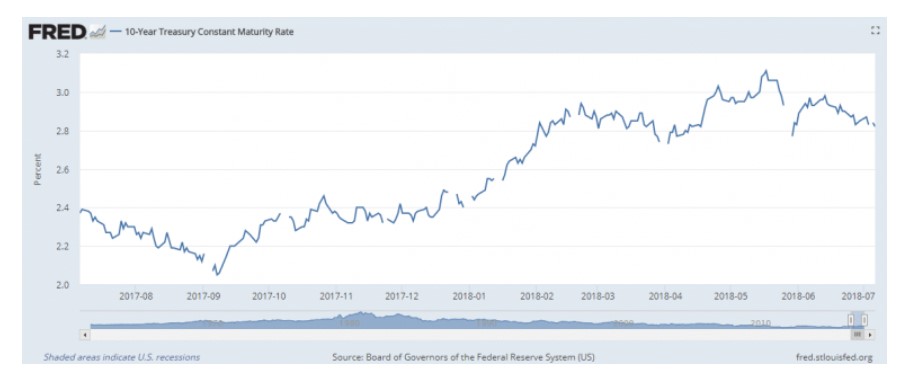

The stock market has been crazy this week and a large part of it has to do with the interest rates rising significantly. A lot of experts watch the 10-Year U.S. Treasury note where rates have jumped from 2.46% to 2.84% in the first 30 days of the year. That is a massive jump for a somewhat stable security and as a result has some people worried.

Now, the 10-Year U.S. Treasury does NOT directly affect mortgage rates contrary to popular belief (my first job out of college was a mortgage broker so I studied this in depth), but the 10-Year is used as a hedge for mortgage investors. Banks and originators of mortgages, use the 10-Year U.S. Treasury note almost as an insurance policy against the true maker of mortgage interest rates known as mortgage-backed securities (MBS).

That all said, the 10-Year and MBS move in a positive correlation and can influence each other indirectly.

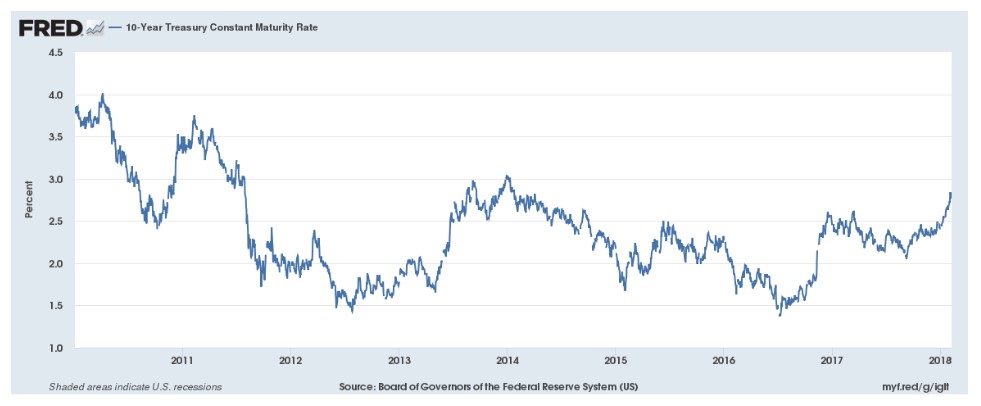

Take a look at the 10-Year chart since 2010…

Now, take a look at the 30-Year Fixed Mortgage Rate in the same time frame…

Pretty dang similar, right?

The 30-Year Mortgage Rate

Some of my clients with pre-approvals have seen their projected 30-year rate jump from 4.125% to 4.5% in a just two weeks! I am writing this blog to give a slight history lesson so you can make mortgage decisions for yourself and how I am advising my clientele.

Let’s look at the 30-year mortgage rate graph and the high made each year…

2018: 4.32%

2017: 4.30%

2016: 4.32%

2015: 4.09%

2014: 4.53%

2013: 4.58%

2012: 4.08%

2011: 5.05%

2010: 5.21%

For the last three or four years we have hit a high of right about where we are now. The recovery years of 2013 and 2014 were higher at 4.5% and the South Bay market was very hot during those years.

Now of course, today’s property prices are higher so rising interest rates might have more of an impact, however, one can argue that the economy is growing, wages are going up, tax reform will deliver wealth (if only short term), and Millennials are coming of age to buy homes. Sure, going above rates seen over the past few years might be painful but currently everything is fine. In short, it just sucks for buyers when we were at 3.78% this past September and are now at 4.32%. Ouch!

For now, this “rate tantrum” is merely psychological because of the run up in the short term. When you look at the numbers over the long term, things are not so bad.

The 7-Year Fixed Mortgage Rate

Since rates do not feel as good as September, I am recommending to clients that they look into 5-year and 7-year fixed rates as they are lower than the 30-year rate. There are a few reasons to my game plan…

1. If you look at the charts, rates move higher and lower throughout the year. There is a potential that rates go back down to 4% or maybe even 3.78%. Enjoy your lower short term fixed rate and if rates drop again, you can refinance into a 30-year rate.

2. On the flip side, if rates continue to go higher, your rate is going to be significantly discounted to the rest of the market. Hang tight, especially if you are not planning to have your home as a “forever” home.

Now, you might be thinking…what if rates go higher and in five years I go adjustable?

3. First and foremost, most of these adjustable-rate mortgages (ARM) have a max ceiling of 5% higher than your start rate. In five years, could you handle that rate and/or have savings to pay off your loan? That is worst case scenario.

For me, here is what really might happen…

4. If rates continue to go up, that means housing prices can support higher rates and likely will continue to go up. In the late 70’s into 80’s, inflation was high and rates were climbing…but so were housing prices. My belief that if rates surge then housing prices will surge. If you cannot support your mortgage in five years, then your house is likely worth much much more and you can sell at a nice profit and then become a renter if needed.

5. Or, if housing price tumble The Fed will lower rates, start quantitative easing again and rates will go back to 3% or less. Your house might be worth less but as long as you can support the payment now, you can almost assuredly refinance into a much much more affordable rate and thus, lower your housing nut.

Conclusion

For those that are not full time real estate professionals, please consult with your CPA, financial advisor, lender, and real estate agent when considering short-term fixed rates. You need to know Plan B, C, D, etc. if there is a change in the economy and make sure you know can take the proper precautions. That said, there is risk in going with a short term rate but I genuinely feel there are more positive outcomes than negative ones. Just prepare for worst case scenario and hope the positive scenarios come to fruition. If you get the positive outcome, then your wallet and net worth will thank you!